At the heart of BNPL’s promise of “interest-free” shopping lies a financial sleight of hand, and someone always pays. That someone, more often than not, is you, whether you clicked “pay in 4” or not. A Buy Now Pay Later (BNPL) is a type of installment loan which allows you to purchase something with little to no initial payment and pay off the balance over four or fewer payments. What began as a small fintech idea has quietly become a staple for everyday Australians, reflected in the BNPL market’s impressive 25.1% compounded annual growth between 2022-2025, and its expectation to hit US$18.34 billion by the end of 2026. But convenience, it turns out, comes at a price.

The model is deceptively simple. Rather than charging consumers interest, BNPL providers extract their revenue directly from merchants. Afterpay charges merchants a 4–6% commission plus 30 cents per transaction, while Klarna levies between 3.29% and 5.99% plus 30 cents. For context, a typical credit card transaction costs businesses 2% to 3% in processing fees. A BNPL transaction? 5% to 8% — a substantial increase in cost per sale. The gap is stark, and it does not simply evaporate into thin air. BNPL providers can afford to offer interest‑free financing for one simple reason: they charge merchants hefty fees. And in the tight‑margin world of retail, those costs rarely disappear quietly. As BNPL fees climb, nearly one in three retailers end up passing the expense on to shoppers through higher prices at checkout. The irony is hard to miss. A product marketed as a tool for affordability is, in practice, contributing to price inflation for the very consumers it claims to help.

Afterpay advertisement (Source: ABC)

This creates what economists describe as a price discrimination mechanism. Merchants charge regular retail prices to customers who do not use BNPL — those who are less price-sensitive and provide a subsidy in the form of an interest-free short-term loan to customers who use BNPL, those who are more price-sensitive. In plain terms: cash-paying customers quietly cross-subsidize the BNPL users beside them in the checkout queue. It is a hidden tax, levied on the financially disciplined to fund the financially fragmented. For small businesses, the picture is even more troubling. According to Finaloop’s 2025 analysis of 2,500 e‑commerce stores, 63% of merchants view BNPL fees as a serious threat to their profitability. Many report needing product margins of at least 25–30% simply to absorb these costs without eroding revenue. For those operating below that threshold, the choice becomes stark: raise prices, or step away from BNPL altogether.

Capital One’s CEO Richard Fairbank perhaps put it most bluntly, observing that BNPL providers take substantial margins on each purchase and that “the elephant in the room is the sustainability of the merchant subsidy.” Indeed, the system’s sustainability rests on a foundational tension: merchants fund interest-free credit for consumers, consumers fund merchants through inflated prices, and BNPL platforms profit from both ends. It is not a revolution in consumer finance. It is a redistribution, and the bill, as always, finds its way back to the ordinary shopper.

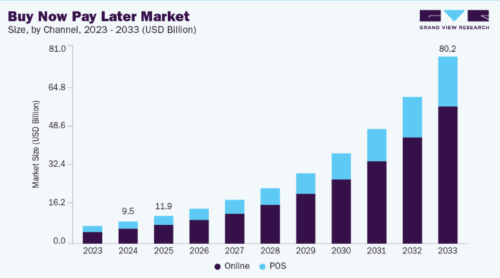

Buy Now Pay Later Market Size, Share, Trends Report, 2033 (Source: Grand View Research)

Arguably, these services’ greatest appeal is the low barriers to consumption. Because payments are separated into more digestible quantities for bank accounts, it temporarily postpones the pain associated with a declining balance for its owners. However, by doing so, it subtly builds an illusion that products are cheaper than they are. A pair of $200 Onitsuka Tiger Mexico 66 sneakers only costs me $50 today. Where does the remaining $150 go? Forgotten, in the pile of other fragmented, future obligations. This affordability perception is particularly concerning for young consumers, who are constantly enticed by new fashion or technology trends, despite their elementary-level financial literacy. What was a want, now becomes a need.

BNPL companies have not only perfected a recipe to fuel overspending, but more unsettlingly, a disguised scheme for debt accumulation. Heavily marketed with key terms “pay in 4” or “interest-free”, it masks the reality of BNPL as a form of credit, where the attention is diverted to its convenience rather than a genuine borrowing system.

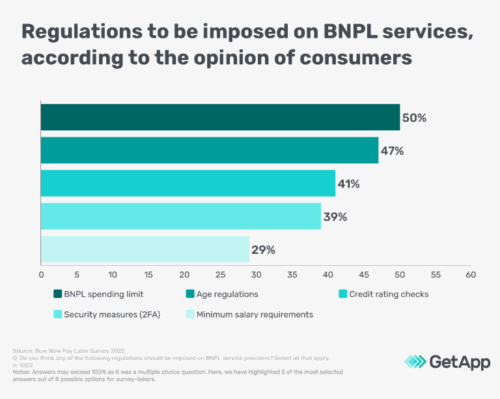

What do customers think of the new regulations? (Source: Get App)

Progressively, the aggregation of mindless clicks on apps, such as Afterpay and Klarna, has reshaped spending habits, resulting in a ticking time bomb for consumers. Like most things, missed payments do not come for free. Late fees can even be more costly than credit card interest. Curtin University’s Dr Lien Duong discovered that Afterpay charged fees equivalent to a credit card interest rate of 28.28%, well above the average interest rate of 22% on a typical credit card. Extending beyond immediate financial penalties, repeat late offenders are in jeopardy of diminished creditworthiness, quietly closing the doors to future borrowing opportunities. A particular concern for young users, who are establishing their financial reputation. Any misstep could be the difference between $6000 and $4000 monthly mortgage repayment, or even being priced out of the market entirely.

Although for some, BNPL is not a choice, but a means of survival. The rising cost-of-living crisis has 51% of Australians handing food, fuel and utilities bills to BNPL services as a last resort. What began as an instant gratification instrument for discretionary goods over manageable payment cycles transformed into a coping mechanism to ease payment loads for everyday essentials. In essence, these financially-vulnerable users’ dependence has triggered a “debt spiral”, where short-term cash relief paves a long-term pathway of poor financial health. It is a dangerous game that BNPL users are playing, with the chance of winning — slim to nothing.

For years, Buy Now Pay Later providers operated in a regulatory blind spot. Unlike credit cards or personal loans, BNPL products were exempt from the National Consumer Credit Protection Act 2009. This means that providers don’t face any responsible lending standards and require no Australian Credit License, thus creating an unintended regulatory gap which can potentially lead to consumer harm. This harm is evident as shown by a Good Shepherd survey in 2022 which found that 84% of financial practitioners reported that their clients had attempted to manage BNPL debt by opening additional BNPL accounts, leading to compounding debt and an unmanageable debt spiral. In response to this crisis, the government launched a formal consultation, where Minister Stephen Jones asserted that BNPL’s credit-like nature means that it should not be exempted from the National Credit Act.

Designed for ease, not reflection (Source: Choice)

That stance was officially legislated in November 2024, and effective starting from 10 June 2025, when the Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024 brought all BNPL products under the National Consumer Credit Protection Act, with ASIC’s Regulatory Guide 281 outlining the modified responsible lending obligations required for all BNPL providers, some obligations include mandatory affordability checks and disclosure requirements. Most crucially, BNPL providers are also expected to hold a credit license by 10 June 2025 if they intend to continue their credit activities involving BNPL contracts.

For the first time, BNPL users also gained access to the Australian Financial Complaints Authority (AFCA) for external dispute resolution, in accordance with the ASIC RG 281. This marked a significant positive shift in consumer protection that had long been missing from the sector. That being said, the regulatory landscape remains incomplete. While the RBA confirmed a ban on credit and debit card surcharges from 1 October 2026, BNPL products still sit outside of the prohibition. Providers like Afterpay still contractually forbids merchants from passing their fees directly to BNPL-using consumers, forcing merchants to absorb the cost in their overall pricing and resulting in all Australians bearing the burden of higher costs. However, a further consultation is planned for mid-2026 to address this exact issue.

Flexibility is no longer a luxury. In a cost-of-living crisis, it has become a lifeline. High living costs have kept demand for short-term, low-cost credit strong, and BNPL has answered that call loudly. But as it deepens its integration into digital wallets, mortgage assessments, and everyday checkouts, credit is becoming less a conscious decision and more an ambient condition, invisible, ever-present, and quietly consequential. The real question is no longer whether BNPL is here to stay. It is whether consumers will notice it at all.

Sources:

https://www.consumerfinance.gov/ask-cfpb/what-is-a-buy-now-pay-later-bnpl-loan-en-2119/

https://www.researchandmarkets.com/report/australia-buy-now-pay-later-market

https://primer.io/blog/klarna-vs-afterpay-for-merchants

https://www.hbs.edu/ris/Publication%20Files/Buy%20now,%20pay%20later%20credit_EW_a84b3c98-3608-4f28-a534-8545246ac522.pdf

https://www.bain.com/globalassets/noindex/2021/bain_report_buy_now_pay_later-in-the-uk.pdf

https://www.richmondfed.org/publications/research/economic_brief/2025/eb_25-03

https://emacintl.com/bnpl-merchant-fees-how-installments-are-reshaping-retail-profit-margins

https://www.reuters.com/business/finance/capital-one-test-buy-now-pay-later-product-this-year-ceo-says-2021-09-13/

https://www.bcu.com.au/the-money-mindset/is-buy-now-pay-later-really-cheaper-than-using-a-credit-card/

https://newsroom.au.paypal-corp.com/gen-z-leads-bnpl-growth-paypal-pay-in-4-2025

https://treasury.gov.au/consultation/c2022-338372

https://ministers.treasury.gov.au/ministers/stephen-jones-2022/media-releases/government-introduces-consumer-protections-buy-now-pay

https://www.nortonrosefulbright.com/en/knowledge/publications/a6cfa71f/bnpl-compliance-countdown

https://www.ashurst.com/en/insights/financial-services-snapshots-6232025-73449-am/

The CAINZ Digest is published by CAINZ, a student society affiliated with the Faculty of Business at the University of Melbourne. Opinions published are not necessarily those of the publishers, printers or editors. CAINZ and the University of Melbourne do not accept any responsibility for the accuracy of information contained in the publication.